A comprehensive expenses policy is one of the pillars of good governance for a council. It should balance the need for rigorous process, value for money and efficiency in decision making to ensure councils continue to function in accordance with community expectations. In order to address these requirements, the policy should be reviewed at least once in each financial year.

Council expenses policies and procedures need to provide transparency and accountability of councillor expenses and help mitigate corruption risks. Council policies that promote these outcomes clearly specify:

- what types of councillor expenses council will reimburse. This must include at a minimum the categories of expenses identified in the 2014 Regulations and in the Act,29 together with any other types of expenses a council considers are reasonably incurred while carrying out the duties of councillor

- what form is to be used to make a claim for reimbursement and what information is required to be included in a claim form in support of the claim. Council business should be clearly defined and the purpose of the expense and how it relates to the duties of a councillor should be included

- what documentary evidence is required in addition to the claim form. For example, a GST tax invoice, receipts, logbook entries or a report regarding training attended

- council personnel involved in the claims process and what each of their roles and responsibilities are, such as who is responsible for completing the claim form and providing supporting evidence, checking the legitimacy of the claim, authorising the expense, and processing the reimbursement

- the date for lodgement of reimbursement claims, for example, within one month of incurring the expense or by a certain day of each month;

- how reimbursements will be provided to councillors, such as on a monthly basis by electronic funds transfer

Early in 2020, Local Government Victoria sought feedback on council expenses policies and working with councils on best practice for a policy.30 In June 2020, LGV published a draft Council Expenses Policy, with the aim of refining this draft policy as further feedback was received from councils.

The draft policy aims to apply sections 40 and 41 of the Act in a policy framework by setting out:

- criteria for the reimbursement of out-of-pocket expenses

- requirement to reimburse carer and dependent- related expenses

- requirement to provide the details of expenses reimbursements to council’s Audit and Risk Committee; and

- procedures to be followed in applying for and making reimbursements of expenses

While the draft policy specifies that childcare and carer’s expenses are qualifying expenses as required under the Act it mainly provides broad advice on reimbursement procedures and requires councils to apply their own judgment on what should be included in their policy.

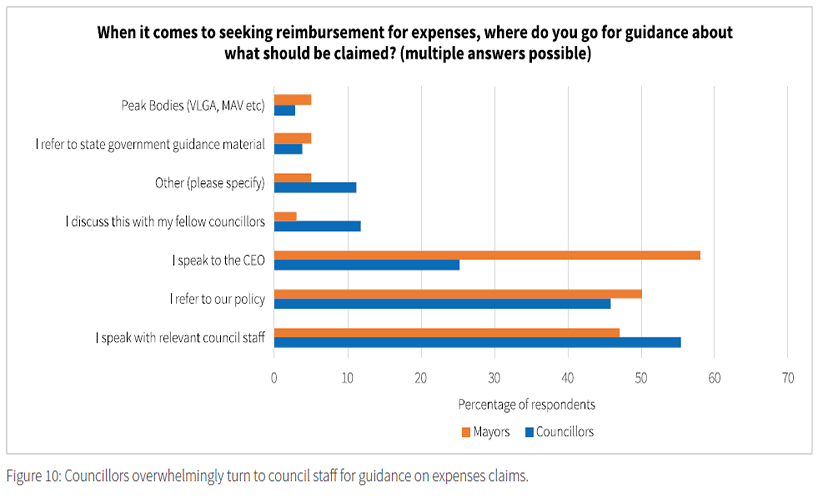

Based on feedback received by the Inspectorate through its surveys and discussions with council governance staff, councils want guidance on the content of their expenses policies, including:

- what kinds of expenses are and are not reimbursable, with questions such as whether councillor produced ward newsletters, or buying alcohol or meals for other persons should qualify for reimbursement

- whether caps should apply to certain categories of expenses, such as attendance at conferences and training

- whether there should be a time limit on the submission of claims for reimbursement; and

- who should approve expense reimbursement claims

The Inspectorate’s review of council expenses policies showed variation in matters including the extent of entitlements, based on differences in the rates of reimbursement (e.g. for kilometres travelled) and whether caps are in place for certain types of expenditure, and if they are, the amount of them. The biggest variation exists in relation to professional development and training caps, while other councils have caps for items such as meals and childcare rates.

A ‘better practice’ template policy for councillor expenses and facilities was developed by the NSW Office of Local Government in 2017.31 The template policy addresses areas similar to those in which council governance staff are seeking further guidance. For example, the template policy suggests councils devise caps for certain categories of expenses, specifies what types of memberships of professional bodies will be reimbursed, and states that councillors will not be reimbursed for alcoholic beverages. Victorian councils would be assisted by a similarly detailed model template for an expenses policy, which can be modified to meet their individual needs.

In addition, an accompanying model claim form and expense reimbursement procedure document would greatly assist councils. The use of such documents would encourage standardisation of entitlements across councils and quell uncertainty within councils regarding the content of their policies.

Section 41(2) of the Act requires the Council Expenses Policy to specify the expenses reimbursement procedures and LGV’s draft policy provides an example of what these procedures may look like. The 7 audited councils largely did not capture relevant procedures, such as how claims are processed and who is involved in the process, in their policies or in a stand-alone document. Instead, they relied upon staff to share knowledge regarding how things are done.

While there is no requirement for a standalone procedural document, it would be best practice for councils to have such a document. Strathbogie Shire Council developed an expense reimbursement procedure document to accompany their councillor expenses policy, which they amended following a review by the Victorian Auditor-General’s Office in 2018-19. According to council governance staff, this procedural document has improved compliance with and understanding of the expenses policy.

29. Sections 41(2)(c), (d) of the Local Government Act 2020

30. See the Local Government Victoria engage site for more information

31. Policy and guidelines available on the OLG website

Updated